ACADEMICS [ PCM | PCB ] Class 11-12th | IIT-JEE | NEET | CUET 2026 | COMPETITIVE EXAMS

Accounts | Economics | Business

450+ Hrs. of Extensive Studies for Accounts, Economics and Business Studies with aprox. 150+ Hrs. devoted on each subject. Along with this Class Tests, Assignments, Doubt Sessions, Syllabus Revision in the end also included. Our expert faculties are Masters Qualified in their specialized subject and having more than 10+ years of experience and expertise to provide in depth knowledge for the subject concerned.

Senior Secondary stage of school education is a stage of transition from general education to discipline-based focus on curriculum. The present updated syllabus keeps in view the rigor and depth of disciplinary approach as well as the comprehension level of learners. Due care has also been taken that the syllabus is comparable to the international standards.

Pattern of Studies

● Interactive Classes

● Home Assignments

● Class Notes

● Periodic Class Tests

● Student's Monthly Report

● One to One Attention

● Doubt Classes

● Syllabus Revision

Report Analysis Parameters

● Tests Marks

● Attendance

● Class Discipline

● Class Response

● Home Assignments

● Student's Comparison with Class

● Last 3 Months Performance

● Special Remarks

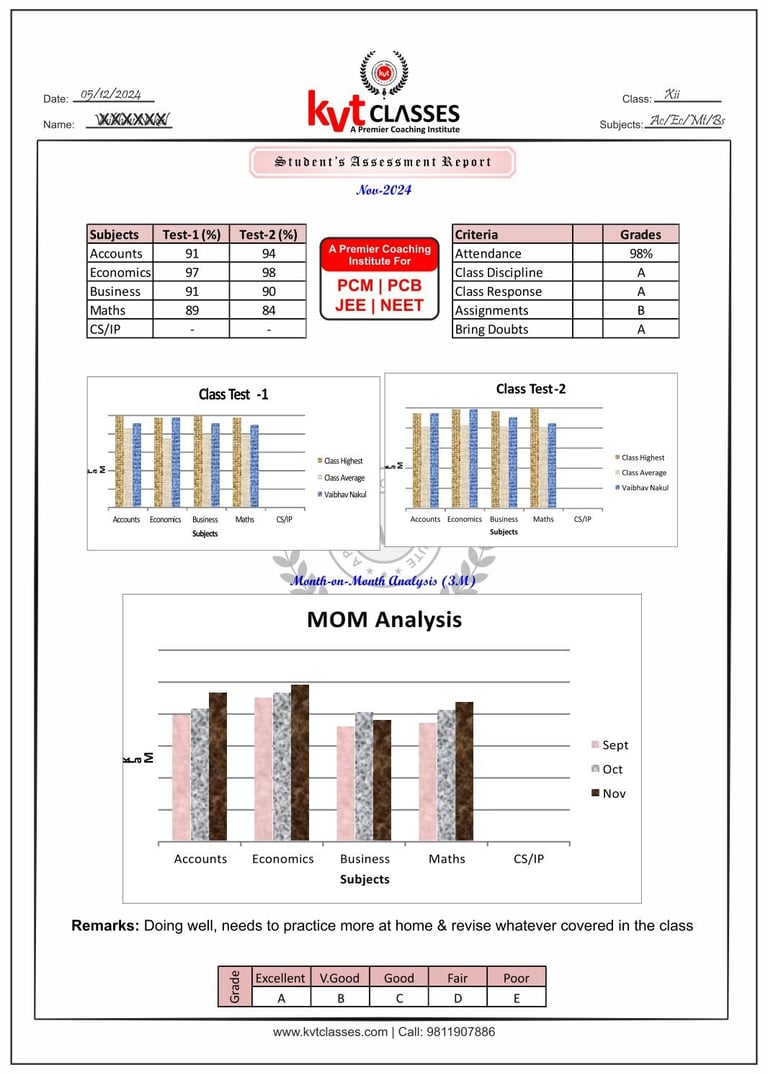

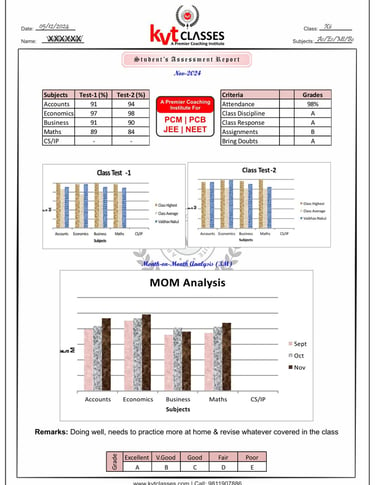

Student's Sample Report

Class Tests

● Two tests per subject in a month

● Test schedule on Saturday in extra hours

● Result within 1 week of test conduct

● Test discussion on result day

● Mistakes rectification briefing

Class-XI

Trusted by Many Prestigious School Students

Students from many prestigious Schools in the vicinity trusted KVT Classes for their Education needs because we believe in giving Quality Education. We get students all across South Delhi who study in different Schools mentioned below..

Star Performers KVT

Students who made us proud

Conduct of Classes

● On board explanation with notes

● Make Concept clear with practical examples

● Interactive class sessions

● Home work / Assignment at the end of the class

● Home work / Assignment check in the next class

● Quick recap of previous class in the next class

● Two tests per month/subject on Saturdays

● Class duration 1 Hr/sub alternate days (3Hrs./wk)

● Extra classes provided when needed

Classes Schedule 2024-25

Commerce Students Class XI-XII

Note: Class Tests will be conducted on Saturday in extra hours

Syllabus & Marks Weightage [ Accounts ]

Syllabus & Marks Weightage [ Economics ]

Syllabus & Marks Weightage [ Business ]

Detailed Syllabus [ Accounts ] XI

PART A: FINANCIAL ACCOUNTING - I

Unit-1: Theoretical Frame Work

Introduction to Accounting

• Accounting- concept, meaning, as a source of information, objectives, advantages and limitations, types of accounting information; users of accounting information and their needs. Qualitative Characteristics of Accounting Information. Role of Accounting in Business.

• Basic Accounting Terms- Entity, Business Transaction, Capital, Drawings. Liabilities (Non Current and Current). Assets (Non Current, Current); Expenditure (Capital and Revenue), Expense, Revenue, Income, Profit, Gain, Loss, Purchase, Sales, Goods, Stock, Debtor, Creditor, Voucher, Discount (Trade discount and Cash Discount)

Theory Base of Accounting

• Fundamental accounting assumptions: GAAP: Concept

• Basic Accounting Concept : Business Entity, Money Measurement, Going Concern, Accounting Period, Cost Concept, Dual Aspect, Revenue Recognition, Matching, Full Disclosure, Consistency, Conservatism,

• Materiality and Objectivity

• System of Accounting. Basis of Accounting: cash basis and accrual basis

• Accounting Standards: Applicability of Accounting Standards (AS) and Indian Accounting Standards (IndAS)

• Goods and Services Tax (GST): Characteristics and Advantages.

After going through this Unit, the students will be able to:

• describe the meaning, significance, objectives, advantages and limitations of accounting in the modem economic environment with varied types of business and non-business economic entities.

• identify / recognise the individual(s) and entities that use accounting information for serving their needs of decision making.

• explain the various terms used in accounting and differentiate between different related terms like current and non-current, capital and revenue.

• give examples of terms like business transaction, liabilities, assets, expenditure and purchases.

• explain that sales/purchases include both cash and credit sales/purchases relating to the accounting year.

• differentiate among income, profits and gains.

• state the meaning of fundamental accounting assumptions and their relevance in accounting.

• describe the meaning of accounting assumptions and the situation in which an assumption is applied during the accounting process.

• explain the meaning, applicability, objectives, advantages and limitations of accounting standards.

• appreciate that various accounting standards developed nationally and globally are in practice for bringing parity in the accounting treatment of different items.

• acknowledge the fact that recording of accounting transactions follows double entry system.

• explain the bases of recording accounting transaction and to appreciate that accrual basis is a better basis for depicting the correct financial position of an enterprise.

• Explain the meaning, advantages and characteristic of GST.

Unit-2: Accounting Process

Recording of Business Transactions

• Voucher and Transactions: Source documents and Vouchers, Preparation of Vouchers, Accounting Equation Approach: Meaning and Analysis, Rules of Debit and Credit.

• Recording of Transactions: Books of Original Entry- Journal

• Special Purpose books:

• Cash Book: Simple, cash book with bank column and petty cashbook

• Purchases book

• Sales book

• Purchases return book

• Sales return book

• Journal proper

Note: Including trade discount, freight and cartage expenses for simple GST calculation.

• Ledger: Format, Posting from journal and subsidiary books, Balancing of accounts

Bank Reconciliation Statement:

• Need and preparation, Bank Reconciliation Statement

Depreciation, Provisions and Reserves

• Depreciation: Meaning, Features, Need, Causes, factors

• Other similar terms: Depletion and Amortisation

• Methods of Depreciation:

i. Straight Line Method (SLM)

ii. Written Down Value Method (WDV)

Note: Excluding change of method

• Difference between SLM and WDV; Advantages of SLM and WDV

• Method of recoding depreciation

i. Charging to asset account

ii. Creating provision for depreciation/accumulated depreciation account

• Treatment of disposal of asset

• Provisions, Reserves, Difference Between Provisions and Reserves.

• Types of Reserves:

i. Revenue reserve

ii. Capital reserve

iii. General reserve

iv. Specific reserve

v. Secret Reserve

• Difference between capital and revenue reserve

Trial balance and Rectification of Errors

• Trial balance: objectives, meaning and preparation

(Scope: Trial balance with balance method only)

• Errors: classification-errors of omission, commission, principles, and compensating; their effect on Trial Balance.

• Detection and rectification of errors;

(i) Errors which do not affect trial balance

(ii) Errors which affect trial balance

• preparation of suspense account.

After going through this Unit, the students will be able to:

• explain the concept of accounting equation and appreciate that every transaction affects either both the sides of the equation or a positive effect on one item and a negative effect on another item on the same side of accounting equation.

• explain the effect of a transaction (increase or decrease) on the assets, liabilities, capital, revenue and expenses.

• appreciate that on the basis of source documents, accounting vouchers are prepared for recording transaction in the books of accounts.

• develop the understanding of recording of transactions in journal and the skill of calculating GST.

• explain the purpose of maintaining a Cash Book and develop the skill of preparing the format of different types of cash books and the method of recording cash transactions in Cash book.

• describe the method of recording transactions other than cash transactions as per their nature in different subsidiary books .

• appreciate that at times bank balance as indicated by cash book is different from the bank balance as shown by the pass book / bank statement and to reconcile both the balances, bank reconciliation statement is prepared.

• develop understanding of preparing bank reconciliation statement.

• appreciate that for ascertaining the position of individual accounts, transactions are posted from subsidiary books and journal proper into the concerned accounts in the ledger and develop the skill of ledger posting.

• explain the necessity of providing depreciation and develop the skill of using different methods for computing depreciation.

• understand the accounting treatment of providing depreciation directly to the concerned asset account or by creating provision for depreciation account.

• appreciate the method of asset disposal through the concerned asset account or by preparing asset disposal account.

•appreciate the need for creating reserves and also making provisions for events which may belong to the current year but may happen in next year.

• appreciate the difference between reserve and reserve fund.

• state the need and objectives of preparing trial balance and develop the skill of preparing trial balance.

• appreciate that errors may be committed during the process of accounting.

• understand the meaning of different types of errors and their effect on trial balance.

• develop the skill of identification and location of errors and their rectification and preparation of suspense account.

Part B: Financial Accounting - II

Unit 3: Financial Statements of Sole Proprietorship

Financial Statements

Meaning, objectives and importance; Revenue and Capital Receipts; Revenue and Capital Expenditure; Deferred Revenue expenditure. Opening journal entry. Trading and Profit and Loss Account: Gross Profit, Operating profit and Net profit. Preparation.

Balance Sheet: need, grouping and marshalling of assets and liabilities. Preparation. Adjustments in preparation of financial statements with respect to closing stock, outstanding expenses, prepaid expenses, accrued income, income received in advance, depreciation, bad debts, provision for doubtful debts, provision for discount on debtors, Abnormal loss, Goods taken for personal use/staff welfare, interest on capital and managers commission. Preparation of Trading and Profit and Loss account and Balance Sheet of a sole proprietorship with adjustments.

After going through this Unit, the students will be able to:

• state the meaning of financial statements the

• purpose of preparing financial statements.

• state the meaning of gross profit, operating profit and net profit and develop the skill of preparing trading and profit and loss account.

• explain the need for preparing balance sheet.

• understand the technique of grouping and marshalling of assets and liabilities.

• appreciate that there may be certain items other than those shown in trial balance which may need adjustments while preparing financial statements.

• develop the understanding and skill to do adjustments for items and their presentation in financial statements like depreciation, closing stock, provisions, abnormal loss etc.

• develop the skill of preparation of trading and profit and loss account and balance sheet.

Incomplete Records

Features, reasons and limitations.

Ascertainment of Profit/Loss by Statement of Affairs method. (excluding conversion method)

Detailed Syllabus [ Economics ] XI

Part A: Statistics for Economics

In this course, the learners are expected to acquire skills in collection, organisation and presentation of quantitative and qualitative information pertaining to various simple economic aspects systematically. It also intends to provide some basic statistical tools to analyse, and interpret any economic information and draw appropriate inferences. In this process, the learners are also expected to understand the behaviour of various economic data.

Unit 1: Introduction 10 Periods

What is Economics?

Meaning, scope, functions and importance of statistics in Economics

Unit 2: Collection, Organisation and Presentation of data 30 Periods

Collection of data - sources of data - primary and secondary; how basic data is collected with concepts of Sampling; methods of collecting data; some important sources of secondary data: Census of India and National Sample Survey Organisation.

Organisation of Data: Meaning and types of variables; Frequency Distribution.

Presentation of Data: Tabular Presentation and Diagrammatic Presentation of Data: (i) Geometric forms (bar diagrams and pie diagrams), (ii) Frequency diagrams (histogram, polygon and Ogive) and (iii) Arithmetic line graphs (time series graph).

Unit 3: Statistical Tools and Interpretation 50 Periods

For all the numerical problems and solutions, the appropriate economic interpretation may be attempted. This means, the students need to solve the problems and provide interpretation for the results derived.

Measures of Central Tendency- Arithmetic mean, Median and Mode

Correlation – meaning and properties, scatter diagram; measures of correlation - Karl Pearson's method (two variables ungrouped data) Spearman's rank correlation (Non-Repeated Ranks and Repeated Ranks).

Introduction to Index Numbers - meaning, types - Wholesale Price Index, Consumer Price Index and index of industrial production, uses of index numbers; Inflation and Index Numbers, Simple Aggregative Method.

Part B: Introductory Microeconomics

Unit 4: Introduction 10 Periods

Meaning of microeconomics and macroeconomics; positive and normative economics

What is an economy? Central problems of an economy: what, how and for whom to produce; concepts of Production Possibility Frontier and Opportunity Cost.

Unit 5: Consumer's Equilibrium and Demand 40 Periods

Consumer's equilibrium - meaning of Utility, Marginal Utility, Law of Diminishing Marginal Utility, conditions of consumer's equilibrium using marginal utility analysis.

Indifference curve analysis of consumer's equilibrium-the consumer's budget (budget set and budget line), preferences of the consumer (indifference curve, indifference map) and conditions of consumer's equilibrium.

Demand, market demand, determinants of demand, demand schedule, demand curve and its slope, movement along and shifts in the demand curve; price elasticity of demand - factors affecting price elasticity of demand; measurement of price elasticity of demand – percentage-change method and total expenditure method.

Unit 6: Producer Behaviour and Supply 35 Periods

Meaning of Production Function – Short-Run and Long-Run

Total Product, Average Product and Marginal Product.

Returns to a Factor

Cost – Short run costs - Total Cost, Total Fixed Cost, Total Variable Cost; Average Cost; Average Fixed Cost, Average Variable Cost and Marginal Cost - meaning and their relationships.

Revenue – Total Revenue, Average Revenue and Marginal Revenue - meaning and their relationship.

Producer's Equilibrium - meaning and its conditions in terms of Marginal Revenue-Marginal Cost.

Supply, market supply, determinants of supply, supply schedule, supply curve and its slope, movements along and shifts in supply curve, price elasticity of supply; measurement of price elasticity of supply - percentage-change method.

Unit 7: Perfect Competition - Price Determination and simple applications. 25 Periods

Perfect competition - Features; Determination of market equilibrium and effects of shifts in demand and supply. (Short Run Only)

Simple Applications of Demand and Supply: Price ceiling, Price floor.

Part C: Project in Economics 20 Periods

Guidelines as given in Class XII curriculum

Detailed Syllabus [ Business Studies ] XI

Part A: Foundation of Business

Concept includes meaning and features

Unit 1: Evolution and Fundamentals of Business

History of Trade and Commerce in India: Indigenous Banking System, Rise of Intermediaries, Transport, Trading Communities: Merchant Corporations, Major Trade Centres, Major Imports and Exports, Position of Indian Sub-Continent in the World Economy

• To acquaint the History of Trade and Commerce in India

Business – meaning and characteristics

• Understand the meaning of business with special reference to economic and non-economic activities.

• Discuss the characteristics of business.

Business, profession and employment – Concept

• Understand the concept of business, profession and employment.

• Differentiate between business, profession and employment.

Objectives of business

• Appreciate the economic and social objectives of business.

• Examine the role of profit in business.

Classification of business activities - Industry and Commerce

• Understand the broad categories of business activities- industry and commerce.

Industry-types: primary, secondary, tertiary Meaning and subgroups

• Describe the various types of industries.

Commerce-trade: (types-internal, external; wholesale and retail) and auxiliaries to trade; (banking, insurance, transportation, warehousing, communication, and advertising) – meaning

• Discuss the meaning of commerce, trade and auxiliaries to trade.

• Discuss the meaning of different types of trade and auxiliaries to trade.

• Examine the role of commerce- trade and auxiliaries to trade.

Business risk-Concept

• Understand the concept of risk as a special characteristic of business.

• Examine the nature and causes of business risks.

Unit 2: Forms of Business organizations

Sole Proprietorship-Concept, merits and limitations

• List the different forms of business organizations and understand their meaning.

• Identify and explain the concept, merits and limitations of Sole Proprietorship.

Partnership-Concept, types, merits and limitation of partnership, registration of a partnership firm, partnership deed. Types of partners

• Identify and explain the concept, merits and limitations of a Partnership firm.

• Understand the types of partnership on the basis of duration and on the basis of liability.

• State the need for registration of a partnership firm.

• Discuss types of partners –active, sleeping, secret, nominal and partner by estoppel.

Hindu Undivided Family Business: Concept

• Understand the concept of Hindu Undivided Family Business.

Cooperative Societies-Concept, merits, and limitations.

• Identify and explain the concept, merits and limitations of Cooperative Societies.

• Understand the concept of consumers, producers, marketing, farmers, credit and housing co-operatives.

Company - Concept, merits and limitations; Types: Private, Public and One Person Company – Concept

• Identify and explain the concept, merits and limitations of private and public companies.

• Understand the meaning of one person company.

• Distinguish between a private company and a public company.

Formation of company - stages, important documents to be used in formation of a company

• Highlight the stages in the formation of a company.

• Discuss the important documents used in the various stages in the formation of a company.

Choice of form of business organization

• Distinguish between the various forms of business organizations.

• Explain the factors that influence the choice of a suitable form of business organization.

Unit 3: Public, Private and Global Enterprises

Public sector and private sector enterprises – Concept

• Develop an understanding of Public sector and private sector enterprises

Forms of public sector enterprises: Departmental Undertakings, Statutory Corporations and Government Company

• Identify and explain the features, merits and limitations of different forms of public sector enterprises

Global Enterprises – Feature Joint venture

Public private partnership – concept

• Develop an understanding of global enterprises, public private partnership by studying their meaning and features.

Unit 4: Business Services

Business services – meaning and types. Banking: Types of bank accounts - savings, current, recurring, fixed deposit and multiple option deposit account

• Understand the meaning and types of business services.

• Discuss the meaning and types of Business service Banking

• Develop an understanding of difference types of bank account.

Banking services with particular reference to Bank Draft, Bank Overdraft, Cash credit. E-Banking: meaning, types of digital payments

• Develop an understanding of the different services provided by banks

Insurance – Principles. Types – life, health, fire and marine insurance – concept

• Recall the concept of insurance

• Understand Utmost Good Faith, Insurable Interest, Indemnity, Contribution, Doctrine of Subrogation and Causa Proxima as principles of insurance

• Discuss the meaning of different types of insurance -life, health, fire, marine insurance.

Postal Service - Mail, Registered Post, Parcel, Speed Post, Courier - meaning

• Understand the utility of different telecom services

Unit 5: Emerging Modes of Business

E - business: concept, scope and benefits

• Give the meaning of e-business.

• Discuss the scope of e-business.

• Appreciate the benefits of e-business

• Distinguish e-business from traditional business.

Unit 6: Social Responsibility of Business and Business Ethics

Concept of social responsibility

• State the concept of social responsibility.

Case of social responsibility

• Examine the case for social responsibility.

Responsibility towards owners, investors, consumers, employees, government and community

• Identify the social responsibility towards different interest groups.

Role of business in environment protection

• Appreciate the role of business in environment protection.

Business Ethics - Concept and Elements

• State the concept of business ethics.

• Describe the elements of business ethics.

Part B: Finance and Trade

Unit 7: Sources of Business Finance

Concept of business finance

• State the meaning, nature and importance of business finance.

Owners’ funds- equity shares, preferences share, retained earnings

• Classify the various sources of funds into owners’ funds.

• State the meaning of owners’ funds.

Borrowed funds: debentures and bonds, loan from financial institution and commercial banks, public deposits, trade credit, Inter Corporate Deposits (ICD)

• State the meaning of borrowed funds.

• Discuss the concept of debentures, bonds, loans from financial institutions and commercial banks, Trade credit and inter corporate deposits.

• Distinguish between owners’ funds and borrowed funds.

Unit 8: Small Business and Enterprises

Entrepreneurship Development (ED): Concept, Characteristics and Need. Process of Entrepreneurship Development: Start-up India Scheme, ways to fund start-up. Intellectual Property Rights and Entrepreneurship

• Understand the concept of Entrepreneurship Development (ED), Intellectual Property Rights

Small scale enterprise as defined by MSMED Act 2006 (Micro, Small and Medium Enterprise Development Act)

• Understand the meaning of small business

Role of small business in India with special reference to rural areas

• Discuss the role of small business in India

Government schemes and agencies for small scale industries: National Small Industries Corporation (NSIC) and District Industrial Centre (DIC) with special reference to rural, backward areas

• Appreciate the various Government schemes and agencies for development of small scale industries. NSIC and DIC with special reference to rural, backward area.

Unit 9: Internal Trade

Internal trade - meaning and types services rendered by a wholesaler and a retailer

• State the meaning and types of internal trade.

• Appreciate the services of wholesalers and retailers.

Types of retail-trade-Itinerant and small scale fixed shops retailers

• Explain the different types of retail trade.

Large scale retailers-Departmental stores, chain stores – concept

• Highlight the distinctive features of departmental stores, chain stores and mail order business.

GST (Goods and Services Tax): Concept and key-features

• Understand the concept of GST

Unit 10: International Trade

International trade: concept and benefits

• Understand the concept of international trade.

• Describe the scope of international trade to the nation and business firms.

Export trade – Meaning and procedure

• State the meaning and objectives of export trade.

• Explain the important steps involved in executing export trade.

Import Trade - Meaning and procedure

• State the meaning and objectives of import trade.

• Discuss the important steps involved in executing import trade.

Documents involved in International Trade; indent, letter of credit, shipping order, shipping bills, mate’s receipt (DA/DP)

• Develop an understanding of the various documents used in international trade.

• Identify the specimen of the various documents used in international trade.

• Highlight the importance of the documents needed in connection with international trade transactions

World Trade Organization (WTO) meaning and objectives

• State the meaning of World Trade Organization.

• Discuss the objectives of World Trade Organization in promoting international trade.